Over the past twenty years, U.S. fruit consumption has declined, but the bigger shift has been in how Americans consume fruit. Eating patterns have shifted toward items that are fresher, less processed, and more aligned with health-oriented routines. The most notable change has been the sharp reduction in juice consumption. Since 2000, juice consumption has declined by 43%, significantly reducing the role of processed formats in overall fruit intake.

By Eda Kocakarin, Jackie Zhang and Ozan Ozaskinli

Executive Summary

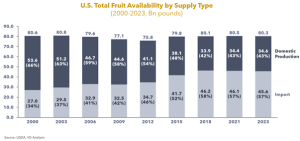

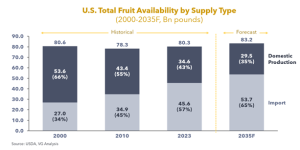

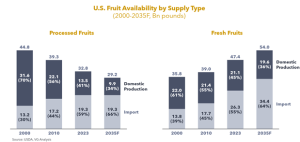

During this same period, the structure of U.S. fruit supply has changed considerably. The availability of fruit grown or processed domestically has narrowed significantly, with overall fruit supply declining by 19 billion pounds since 2000. At the same time, imports have become an increasingly central source of fruit supply, with import share rising from 34% of total availability in 2000 to 57% by 2023, reflecting structural constraints on U.S. production capacity.

Looking ahead to 2035, fresh consumption is projected to increase by 8%, while processed fruit consumption is expected to decline by 15%, leaving overall fruit intake broadly stable as these trends offset each other. On the supply side, domestic fruit production is expected to decline from 34.6 billion pounds in 2023 to 29.5 billion pounds by 2035, while imports will account for a growing share of total supply.

These shifts carry distinct implications for industry participants. For processors, the continued contraction of processed demand, combined with rising reliance on imported inputs and higher domestic processing costs, creates growing pressure on operating models and sourcing strategies. Distributors, in contrast, must manage a more complex and globally oriented fresh supply chain, yet they also gain access to higher-margin opportunities as fresh volumes grow.

1. Consumer Behavior and Demand Transformation

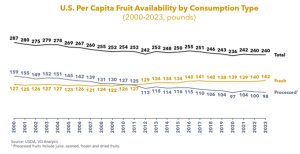

Consumers incorporate fruit into their diets in a variety of ways, choosing among fresh, frozen, dried, canned, and juice formats depending on convenience, preference, and lifestyle. In the early 2000s, this mix was weighed more heavily toward processed fruit, especially with fruit juice.

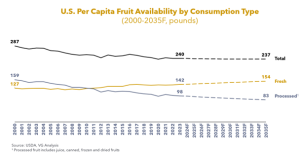

Over the past two decades, the structure of fruit intake in the U.S. has changed notably. Fresh fruit has steadily expanded its share, while processed categories have shrunk. Total per capita fruit availability has fallen by about 20 percent since 2000. Following the sharp decline that occurred from 2000 through the early 2010s, per capita fruit intake has remained relatively stable for nearly a decade, indicating that the major adjustment in total consumption occurred earlier.

Yet despite this overall decline, the share of intake coming from fresh fruit continues to rise, indicating that fresh formats have become increasingly preferred by American consumers.

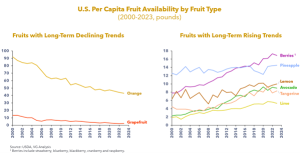

The long-term shift in fruit consumption becomes more distinct when examining trends at the individual fruit level.

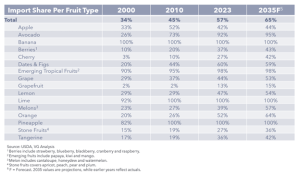

Over the last 20 years, oranges and grapefruits have seen their total consumption fall by nearly half, with declines occurring in both fresh and processed forms in a similar pattern. This contraction reflects a broader reduction in juice consumption habits as well as recurring supply shortages that have constrained availability in recent years.

In contrast, several fruits have expanded across multiple formats. Key citrus varieties such as lemons, limes, and tangerines have shown consistent increases in both fresh and processed consumption. Berry varieties, including blackberry, blueberry, cranberry, raspberry, and strawberry, have also experienced significant growth, with total consumption approximately doubling, supported by strong gains in fresh formats. Pineapples have followed a similar positive trajectory with strong growth on the fresh side, and avocados have expanded almost entirely through higher fresh consumption.

Taken together, these diverging fruit-specific patterns highlight that the national shift toward fresh fruit is being boosted by a distinct set of fruits that have gained importance, while others have steadily lost ground.

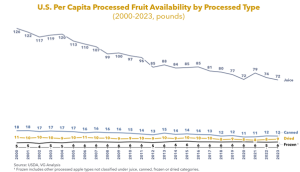

Beyond fruit-specific patterns, it is also important to examine how processed fruit consumption has evolved over time. Juice represents the largest share of processed fruit consumption in the U.S. (79%), so long-term shifts in processed-fruit demand have been driven largely by juice consumption trends. Between 2000 and 2023, per capita juice consumption declined by 43%. Despite this decline, juice remained the dominant processed format in 2023, accounting for 73% of processed fruit consumption.

Canned fruit has also declined materially over the same period, with per capita consumption falling by 32%.

Dried fruit consumption has declined as well, following a similar downward direction as juice and canned fruit, though with a more gradual slope, declining by 18% over the past two decades.

In contrast, frozen fruit has followed a distinct trajectory, with per capita consumption increasing by 19% between 2000 and 2023, making it the only processed subsegment to show sustained growth over the period.

The observed shifts in fruit consumption patterns—across both fruit types and processed formats—stem from two broad forces that have shaped consumer behavior in the last decade. First, evolving health perceptions and a shift away from processed formats have increased the relevance of fresh fruit in daily diets. Second, improvements in year-round availability have made many fresh fruit categories more consistently accessible than in the past.

Reimagining Health & Wellness

A major factor behind the shift toward fresh fruit is the growing emphasis consumers place on health, nutrition, and natural ingredients. Rising awareness of high sugar levels in juice and the perception of processed formats as less beneficial have pushed many consumers toward whole-fruit options instead. Within this broader health shift, several fruit groups have gained momentum because their attributes align closely with modern wellness expectations.

Berries benefit from strong associations with antioxidants, immunity support, natural sweetness, and their central role in smoothies and breakfast bowls.

Pineapple has grown through its refreshing, naturally sweet tropical profile.

Avocado continues to surge due to its reputation for healthy fats, higher nutrient density, and its seamless fit into contemporary meal occasions such as salads, bowls, and breakfast dishes.

Lemon, lime, and tangerine have also expanded within fresh consumption as consumers increasingly favor natural flavor enhancers, clean-ingredient cooking, hydration-oriented uses, and easy-to-eat citrus snacks. Within this group, tangerines stand out for their easy-to-peel, seedless, kid-friendly format, which positions them as a convenient fresh alternative to traditional oranges.

Together, these health-oriented motivations have become a central driver of the fresh-forward consumption patterns observed today.

Year Round Availability

A second force shaping fresh fruit consumption is the significant improvement in year-round availability enabled by more stable and diversified import supply chains.

Many fruits that were once strongly seasonal are now present on grocery shelves throughout all twelve months, eliminating traditional gaps between domestic harvest cycles and making fresh fruit feel increasingly “non-seasonal” to consumers. In several key categories, monthly import unit values show limited volatility, meaning consumers do not experience sharp seasonal price swings even when supply relies heavily on imports.

This continuity is supported by steady monthly import flows from countries such as Mexico, Guatemala, Costa Rica, and Ecuador, which reliably fill domestic production gaps and prevent seasonal shortages.

As a result, these health-driven preferences and improvements in year-round availability have fundamentally reshaped how American consumers engage with fruit, accelerating a long-term shift toward fresh formats.

The rise of specific fruit categories, along with the decline of others, reflects broader changes in lifestyles, purchasing habits, and access conditions. Understanding this consumer-side transformation provides essential context for examining how the U.S. fruit system has evolved in response, particularly in terms of domestic production dynamics and the expanding role of fruit imports, which are the focus of the next section.

2. Historical Evolution of Fruit Supply

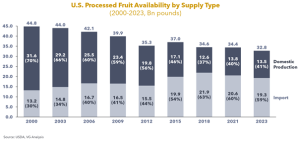

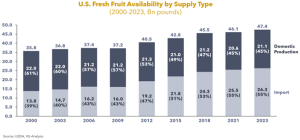

Over the past two decades, the U.S. fruit supply has undergone a major structural realignment—from domestic dominance to heavy reliance on imports. While total fruit demand has been relatively flat, net domestic supply (domestic production minus exports) has fallen by 19 billion pounds since 2000. Imports have filled most of that gap, raising their share of U.S. fruit supply from 34% in 2000 to 57% in 2023, surpassing domestic supply as early as 2015.

At the same time, successive U.S. Farm Bills have remained heavily oriented toward subsidizing major row crops (e.g., corn, soybeans, wheat). Relative to these commodities, fruit producers receive limited financial support and risk protection, which has weakened the sector’s economic footing and reinforced the shift toward import dependence.

Processed Fruits: Import Dependence & Domestic Production Decline

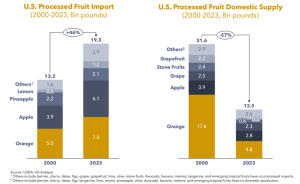

The decline in domestic share is driven primarily by losses in processed fruit. Local processed fruit shrinkage accounts for roughly 95% of the total contraction in overall domestic fruit supply. Farmers have stronger incentives to prioritize the fresh market, where profit margins are typically higher, while lower labor and input costs abroad have made foreign processing more competitive. As a result, the import share of processed fruit rose to 59% in 2023, up from 30% in 2000.

This shift is most visible in apples and oranges, where manufacturing orange juice faces growing challenges in sourcing fruit locally.

Processed apples have decreased 1 billion pounds in domestic supply while increasing 2.2 billion from imports since 2000. Now it has become one of the major imported processed fruits, sourcing primarily from China. With fresh apple prices more than three times higher per unit than apples sold to processors, growers have increasingly allocated production to the more popular fresh channels, leaving the ground for lower-cost imports.

For processed oranges, the pressure is even more severe. Orange juice has decreased 12.8 billion pounds (~70% of total domestic processed decline) in local production while increasing only 2 billion pounds from import. Florida, the primary U.S. orange-producing region, has been hit hard by citrus disease and repeated hurricanes, with bearing acreage down roughly 60% and yields down nearly 80%, shrinking the state’s citrus sector to a fraction of its historical scale. As a result, Brazil has roughly doubled its orange juice export volume to the U.S. and has become the leading supplier.

Fresh Fruits: Import Rise & Domestic Production Defense

On the fresh side, import growth has been led by fast-rising consumption categories with limited domestic production capacity, creating strong incentives for distributors to source abroad.

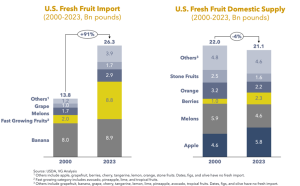

Import reliance in fresh fruit has strengthened significantly, with import share increasing from 39% to 55% between 2000 and 2023. The fresh imports have increased 18.6 billion pounds since 2000, representing almost 70% of total increase in fruit imports.

Avocados, pineapples, limes and tropical fruits (kiwi, papaya, and mango) account for more than half of this increase.

Pineapple and lime domestic production largely disappeared before 2010 due to severe natural disasters and growing feasibility.

Meanwhile, avocado contributes the most to the total fresh import growth: its import share climbed from 26% to 92% in less than 25 years. The U.S. imports more avocados mostly from Mexico, because domestic production, mainly in California, struggles to meet booming demand due to high costs, severe water scarcity, and limited suitable growing regions, while Mexico offers ideal climates (volcanic soil, sun, rain) and economies of scale, allowing for cheaper, year-round supply, especially after NAFTA opened the market.

While domestic fresh fruit supply has remained broadly stable (around 21 billion pounds), growers have increasingly shifted toward higher-return categories to stay competitive against imported fresh fruit. The most prominent example of this shift is berries.

Local fresh berries have grown more than any other fruit group, increasing by nearly 80% over the past 15 years, driven by strawberries and cultivated (tame) blueberries, two categories that have benefited from biological strengths and sustained research investment. Strawberries, the nation’s highest-volume berry, deliver the highest yield of any non-citrus fruit, supported by their flexible plant biology, runner-based propagation, and adaptability across diverse growing conditions. Public breeding programs in California and Florida continue to release improved cultivars with greater disease resistance and longer production windows. Cultivated blueberries share similar advantages: they can be grown successfully in both northern and southern climates and offer strong economic returns, supported by premium pricing and high perceived nutritional value. These production and profitability advantages have encouraged growers to expand acreage and output in both categories.

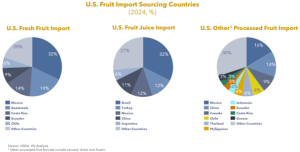

Concentration on Importing Countries

U.S. fruit imports are heavily concentrated among a few key countries, with Mexico and Brazil leading in fresh fruit and juice respectively. Mexico alone represents more than 30% of fresh fruit imports, followed by Guatemala and Costa Rica, underscoring a strong reliance on Latin American sources. For fruit juice, Brazil dominates, while other countries collectively contribute a sizable share. In contrast, other processed fruit imports are far less concentrated, with nearly half coming from a broad mix of other countries, indicating greater global distribution for these products.

In summary, the U.S. fruit supply structure has shifted from domestic dominance toward import diversification. Growth is now concentrated in a few categories capable of withstanding evolving consumer behavior with biological and economic advantages, leaving imports to serve as the primary stabilizer on the supply side and the defining force in the new market balance.

3. Long-Term Outlook for the Fruit Market

Fruit Consumption Outlook

U.S. fruit consumption has followed a recognizable long-term pattern: a sharp decline from 2000 through the early 2010s, followed by nearly a decade of stabilization, a dynamic discussed in detail in the Consumer Behavior section. While total consumption is projected to remain broadly stable through 2035, this outcome reflects divergent trajectories across fresh and processed categories. Projected increases in fresh consumption and declines in processed consumption largely offset each other, even as the structural shift in how Americans consume fruit continues to evolve.

By 2035, total fruit consumption is expected to reach 237 pounds per person per year. Fresh consumption is projected to increase by 8 percent and processed consumption to decline by 15 percent between 2023 and 2035.

To translate these historical patterns into a forward-looking view, a bottom-up forecasting approach was applied to capture category-specific consumption dynamics. The outlook was constructed from 18 fruit groups, formed by clustering USDA-reported categories with similar consumption trends. For each group, fresh and processed consumption were modeled separately, and future import levels were projected using historical patterns from 2000–2023. Forecast models were selected based on best statistical fit and subsequently refined through expert judgment to ensure realistic category trajectories. Taken together, these category-level forecasts form a national outlook that captures the structural changes occurring across individual fruit categories.

Within this overall outlook, growth is expected to remain concentrated in avocados, berries, lemons, limes, tangerines, and pineapples, which continue to show strong and consistent momentum in consumer adoption. These categories are becoming part of everyday eating routines. They influence long-term habits by supporting healthy-fat meals, citrus-based hydration and greater use of whole fruit.

Improvements in convenience, including the expansion of ready-to-eat, precut, and portable offerings, further enable fresh fruit to satisfy many eating occasions that previously favored processed formats. Together, these shifts reinforce the durable consumer movement toward fresh fruit.

Processed fruit consumption is expected to continue declining as behavioral and perception shifts reduce demand for juice and canned formats. The most notable erosion has occurred at breakfast occasions, where juice consumption has steadily fallen and no longer holds its former central role. At the same time, canned fruit has become increasingly misaligned with modern healthy lifestyle expectations, further limiting its relevance in daily eating patterns.

These pressures are particularly pronounced among younger consumers, who often view juice as a high-sugar beverage rather than a fruit serving. Combined with the persistent, multiyear decline in orange juice, these factors reinforce the structural contraction of processed fruit categories and are expected to continue weighing on the segment through 2035.

Fruit Supply Outlook

As recent consumption trends continue, their effects on the supply side are becoming clearer. By 2035, the U.S. fruit supply is expected to become more import dependent as domestic production declines from 34.6 billion pounds in 2023 to 29.5 billion pounds. Over the same period, the import share of total supply is projected to rise from 57% to 65%, reflecting the increasing role of imported fruit in meeting U.S. demand.

Domestic supply is also limited by the types of fruit the U.S. can feasibly produce at scale. Many fruits cannot be grown successfully in the U.S. due to unsuitable climate and soil conditions. For example, production is limited for fruits such as avocados, limes, and pineapples, while demand for berries, tangerines, and lemons is rising faster than new farming area can be brought into production. These structural limits prevent total U.S. production from keeping pace with evolving consumer demand.

Domestic production is playing a progressively smaller role in processed fruit, increasing the segment’s reliance on imports.

About 70% of the projected reduction in domestic fruit supply comes from processed fruit, consistent with the long-term decline in U.S. processing. Domestic processed fruit production is projected to fall from 13.5 billion pounds in 2023 to 9.9 billion pounds by 2035. This decline reflects growers moving toward higher-margin fresh crops and the continued impact of citrus disease and weather-related losses that reduce fruit suitable for juice processing.

Even as import volumes stay close to 19 billion pounds, they make up a growing share of a shrinking processed fruit segment. Import share is expected to increase from 59% to 66% by 2035, largely because of tighter domestic supply rather than expanding imports.

Domestic fresh fruit production is expected to hold its ground through 2035, while growing demand continues to increase reliance on imports.

In line with this broader pattern, domestic fresh fruit production is projected to decline only slightly from 21 billion pounds in 2023 to 19.6 billion pounds by 2035.

The overall fresh fruit domestic supply remains relatively stable, but the mix of fruits produced in the U.S. is changing. Demand is increasingly centered around avocados, berries, lemons, limes, pineapples, and tangerines. Growers are moving land away from slowing categories like melons, oranges, and grapefruit toward crops that offer stronger returns, especially berries, lemons, and tangerines.

However, much of the increase in demand is for fruits the U.S. cannot produce at scale because of climate and growing-condition limits. These shifts change which fruits are grown in the U.S., but they do not increase total fresh production.

As a result, imports will need to cover most of the incremental demand and are expected to rise from 47 billion pounds in 2023 to 54 billion pounds by 2035, raising their share of fresh fruit availability to 64%.

4. Strategic Implications for the Fruit Processors and Distributors

The structure of the U.S. fruit market is being reshaped by recent shifts in consumption and supply. Processed demand continues to decline, fresh preferences are strengthening, and import reliance is increasing. These long-term dynamics create new pressures and opportunities across the value chain, with distinct implications for processors and distributors.

For processors, the decline in processed fruit consumption adds structural pressure to a segment already facing shrinking domestic supply and rising import dependence. As reliance on imported inputs grows, exposure to global price volatility, freight disruptions, and supply chain uncertainty increases.

At the same time, domestic bottling and processing costs in the United States have risen materially. Expenses related to labor, energy, packaging materials, and logistics have increased by roughly 33% over the last 10 years, weakening the cost position of U.S.-based processing operations.

Looking ahead, processors will need to reassess how they compete as the processed fruit market continues to contract. Some may shift toward higher-value or specialized formats to support margins, while others may evaluate alternative sourcing or production configurations if domestic processing becomes structurally less competitive.

In categories with high import exposure and limited growth potential, processors may increasingly need to rationalize their portfolios. This may involve shifting focus away from lower-return segments while reallocating resources toward more resilient or differentiated offerings.

For distributors, rising fresh consumption and increasing import dependence are reshaping operational requirements across the supply chain. As more fresh volume moves through international channels, distributors must manage larger and more complex cold chain networks and meet growing expectations for year-round availability.

This raises exposure to logistics disruptions, higher transportation costs, and spoilage risk, especially as a greater share of national supply flows through ports and refrigerated capacity tightens. Dependence on a limited number of supplying countries also heightens geographic and political vulnerability.

At the same time, these pressures create meaningful opportunities. Fresh distribution typically carries higher margins than packaged goods, strengthening the business case for expanding fresh handling capacity. Distributors can broaden sourcing networks, deepen partnerships with key supplying regions, and scale their role in fast-growing fresh segments.

Overall, the transition toward higher fresh consumption, lower processed demand, and greater import reliance will reshape the commercial landscape for both processors and distributors. Their challenges differ, but long-term success will depend on how effectively they can strengthen supply resilience, adjust sourcing models and align operations with a market increasingly shaped by global supply and fresh-forward consumer behavior.

Authors

Eda Kocakarin

Consultant

Eda.Kocakarin@valuegeneconsulting.com

Jackie Zhang

Business Analyst

Jackie.Zhang@valuegeneconsulting.com

Ozan Ozaskinli

Partner and Managing Director

Ozan.Ozaskinli@valuegeneconsulting.com